Autumn Budget 2024

View

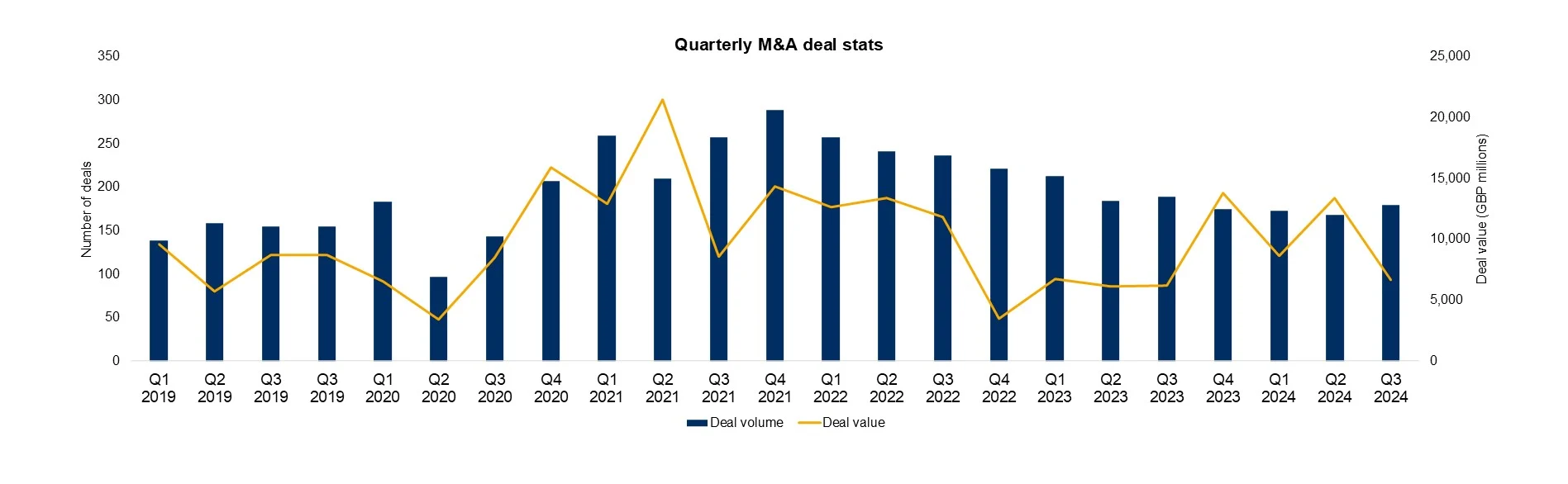

We bring you regular insights to help understand the ever-changing tides and trends within the UK M&A market.

Here we regularly share articles which influence the wider macro circumstances of the UK M&A market and are available to discuss how each of these may impact on your own circumstances and aspirations